Savills Netherlands

winter 2025

A Sustainable Solution to the Housing Shortage

Homeowner Concerns

Introduction

Outlook

Building Upward

Floor Premiums

Follow Us

Savills market intelligence content is designed to engage and immerse users in interactive experiences that are much more captivating than the surface-level, flat reports provided by printable media such as pdfs. Each Savills Netherlands report harnesses the power of a web browser to tell the rich, engaging story of the Dutch real estate market. When printing, you would lose the interactions and animations that make the content a digital experience. In addition, due to our local ESG roadmap, we want to discourage printing as much as possible. Therefore, we don’t offer hard copy or pdf reports anymore.

All content © copyright 2025 Savills. All rights reserved. Savills Nederland Holding B.V., established and registered in the Netherlands. Located: Claude Debussylaan 48, 1082MD Amsterdam. Chamber of Commerce (KvK) number: 33202244.

This Report

Contents

Claude Debussylaan 48, 1082 MD, Amsterdam +31 (0) 20 301 2000

Get in Touch

Savills Beds Special 2024

Dutch Life Sciences

The Office Market of the Future

Logistics Confidence Index 2024

Market in Minutes Q1 2024

Other Reports

Key Findings

Invisible Women in Real Estate

Market in Minutes Q3 2024

STRUCTURAL POTENTIAL AND MARKET REALITY

Market Analysis

Space at the top

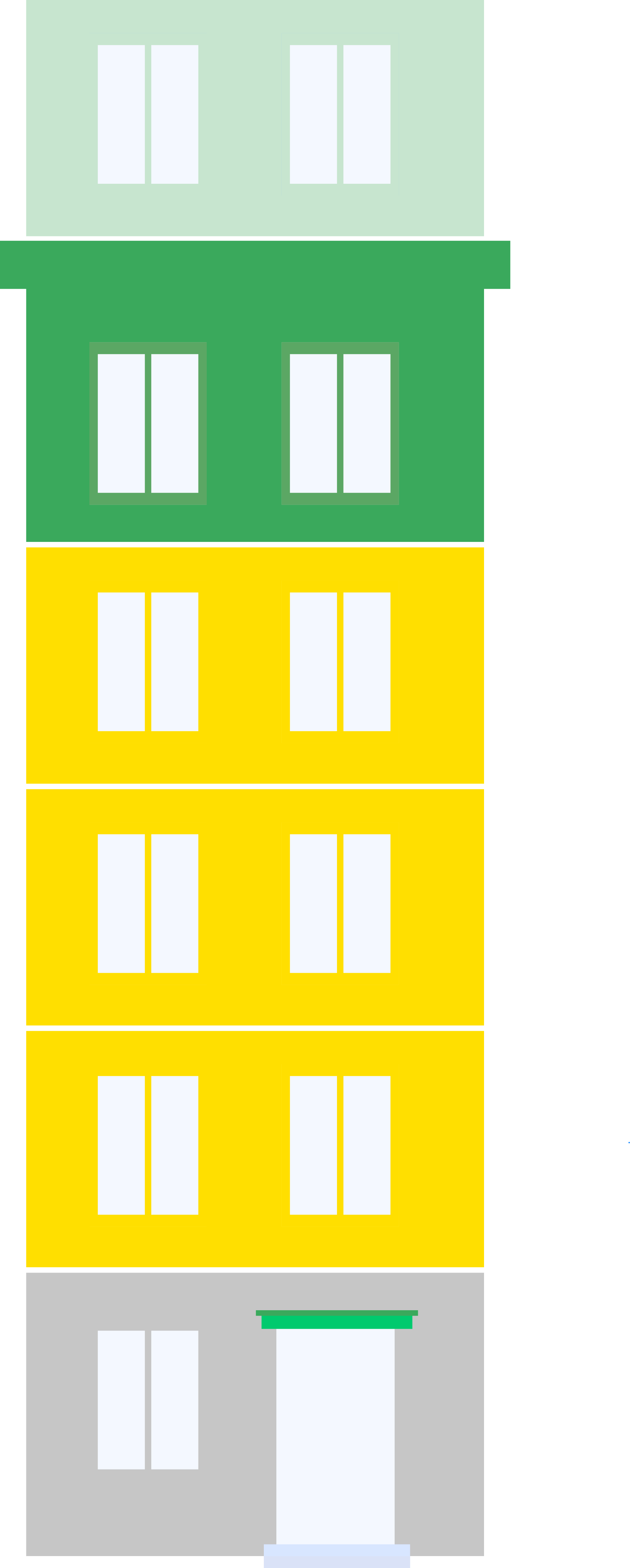

Post-war buildings (1945–1970) with flat roofs and four storeys form a significant part of Amsterdam’s housing stock and provide strong structural and architectural conditions for adding new units. Optoppen could sustainably decrease the housing shortage by 9%.

Optoppen offers substantial potential

The implementation of optoppen can be hindered by top-floor homeowners as they fear a loss in value when their top-floor “exclusivity” disappears after adding an additional floor. Little empirical evidence exists to confirm that this “exclusivity” is factored into the price.

The fear of losing top-floor “exclusivity” prevents full approval from homeowners associations

Adding a fifth floor does not reduce existing top-floor values

Analysis of 1,062 apartment transactions between 2022 and 2025 in post-was buildings shows that price per square metre generally decreases with each additional floor level. The relationship between floor level and price is consistent across both four- and five-storey buildings, indicating, top-floor “exclusivity” is not a price determining factor.

Since typical post-war buildings are originally built without a lift, the floor level premium in our analysis is probably mostly a story about stairs, which explains why higher floors in our dataset are priced lower: the physical effort required to reach them outweighs the benefits for many buyers.

Accessibility, not exclusivity, shapes floor-level pricing

All interviewed lenders assess optoppen positively as a contribution to sustainability and densification efforts. For most lenders, improving sustainability is also a key criteria for financing conditions.

Lenders view optoppen positively

5

4

3

2

1

Adding a fifth floor does not erode existing top-floor prices; accessibility outweighs exclusivity.

Top-floor values hold.

Lenders insights

The Netherlands faces a persistent housing shortage of approximately 395,810 homes, equal to 4.8% of the total housing stock. As pressure on the housing market intensifies, national and municipal policies increasingly emphasise densification and the smarter use of the existing built environment. Optoppen, or roof extensions (adding an additional floor on top of an existing building) is emerging as a scalable and sustainable way to create new homes in well-connected urban neighbourhoods. Although the potential is considerable, regulatory constraints and fragmented ownership hinders development taking off as promised. This research investigates whether top-floor apartments in post-war buildings command a premium per building type and distinguishes perception from actual evidence in Amsterdam. Understanding this dynamic is crucial for Homeowners’ Association (VvE’s) , lenders and developers considering optoppen.

Conclusion

Optoppen is a viable, socially valuable and financeable strategy for expanding housing supply within Amsterdam’s existing neighbourhoods. Combined with energy upgrades and standardised construction approaches, they support urban vitality, improve sustainability and offer a realistic pathway to delivering new homes where land is scarce. With the right partnerships and continued data-led planning, optoppen can play a meaningful role in shaping the future of Amsterdam’s housing market.

All interviewed lenders assess optoppen projects similarly to conventional redevelopment, with strong attention to structural feasibility, VvE consent, and sustainability. However, only some lenders consider optoppen feasible in cases of fragmented ownership.

6

Fragmented ownership is viewed as a critical issue

Why the Netherlands should build upwards

The Netherlands is facing a persistent and structurally high housing shortage. As of 2025, the deficit amounts to approximately 395,810 homes, equal to 4.8% of the total housing stock according to ABF Research. More than double the 2% “healthy” shortage benchmark used by policymakers. Demographic change, ageing housing stock, and limited land availability mean that this shortage is expected to remain significant over the coming decades, despite substantial national efforts to accelerate housing construction. In response to these sustained pressures, current government policy is firmly focused on addressing the structural housing shortage by accelerating new construction. Beyond stimulating new construction, policymakers are pushing the optimisation of existing housing stock through alternative construction methods. These interventions aim to expand housing supply while limiting urban sprawl and making more effective use of existing infrastructure Examples include office-to-residential conversions, co-living concepts, and optoppen, which are expected to expand the housing stock more rapidly and sustainably. To support large-scale neighbourhood development, government policy also aims to invest in supporting infrastructure more efficiently. Public transport, roads, utilities, alongside water safety and climate-adaptive construction must all be in order.

Among all alternative construction methods, optoppen offers significant potential, particularly in neighbourhoods dominated by post-war buildings (1945–1970). These buildings often feature flat roofs, relatively uniform typologies, and structurally suitable designs, making them prime candidates for adding one or more additional floors.

Optoppen can increase housing supply in already well-connected urban areas, support neighbourhood vitality, and present opportunities to improve the energy performance of ageing buildings. However, optoppen remains challenging. While they represent an innovative solution, developers face challenges ranging from lengthy permitting procedures to the requirement of securing full consent from all homeowners within homeowners’ associations (VvE’s).

This research by Savills, in partnership with Creative City Solutions (CCS), examined whether top-floor apartments in post-war buildings in Amsterdam command a price premium and whether adding a fifth floor statistically significantly affects this premium. The research combines an analysis of housing transactions (2022–2025) with the viewpoints of lenders. It aims to provide a data-driven basis for VvE’s, policymakers, developers and lenders considering optoppen projects.

New Homes Above Existing Roofs

The fear of losing top-floor “exclusivity” is raised by top-floor homeowners who fear a loss in value of their home when an additional floor is constructed above them. While top-floor “exclusivity” disappears when an additional floor is added, little empirical evidence exists to confirm that this “exclusivity” affects prices. Do top-floor apartments in post-war buildings actually command a price premium? And if such a premium exists, is it affected when an additional floor is added?

Rethinking Top-Floor Value Myths

Source: Hedwig Heinsman – Tiny Penthouses

Pascale Schellekens

Insight & Data Specialist

By providing a data-driven approach we aim to distinguish perception from evidence to support VvE’s in making informed decisions

Spotlight

Source: Savills & CCs

Value per floor before and after rooftop extension

Floor 3

0

Lower value compared to the ground floor.

Floor 4 (Top floor)

Higher value compared to the ground floor.

Added unit does not reduce the value of the current top floor or any other floor.

Floor 2

Floor 1

Ground Floor

New 5th Floor (optoppen)

BAck to the top

A good example is A.J. Ernststraat 800 in Amsterdam, where Creative City Solutions (CCS) has completed one of its established optoppen projects. Ten sustainable apartments were added on top of an existing post-war building, and the entire building underwent a full renovation. In this specific project, the VvE chose to carry out the sustainability measures at a later stage. The proceeds from the optoppen project were used to replenish the VvE’s reserves, and the portico, balconies, gallery, fire escape and other shared elements were renovated. In addition, the individual owners received a financial payout. The project illustrates how carefully executed optoppen can strengthen both the housing stock and the financial and physical vitality of the neighbourhood, even when sustainability improvements are planned for a later phase.

Case Study

Understanding homeowner concerns

Are top-floor values at risk?

The analysis focuses on post-war buildings (1945–1970) in Amsterdam.

It examines how floor premiums vary across buildings with a maximum of four storeys and buildings with five storeys between 2022 and 2025. Buildings constructed between 1945 and 1970 are examples of typical post-war architecture, of which Amsterdam has many. These buildings have a modest height, flat roofs, and a functional architectural style, which together make it possible to add an additional floor with minimal visual impact.

Source: Creative City Solutions

By analysing whether top-floor apartments within post-war buildings in Amsterdam actually command a premium, and whether such a premium changes when a fifth floor is present, this research aims to separate perception from evidence to support similar implementation such as the above on a larger scale. Understanding this dynamic is essential for homeowners within VvE’s, lenders, and developers considering optoppen.

Climate change is significantly impacting agricultural practices in the Netherlands. Farmers are facing challenges such as unpredictable weather patterns, increased frequency of extreme weather events, and rising sea levels. To combat these issues, Dutch farmers are adopting resilient agricultural practices, such as the use of drought-resistant crop varieties, improved water management systems, and sustainable land-use strategies. Research institutions and government bodies are working together to develop innovative solutions to mitigate the effects of climate change on agriculture.

Real estate implications: Climate-resilient agricultural practices require investment in new infrastructure and technology. Real estate investors and developers should focus on properties that support sustainable and resilient farming methods. This includes irrigation systems, flood defences, and energy-efficient buildings, which can enhance the long-term value and sustainability of agricultural properties. Climate change could also benefit some alternative agricultural sectors, like viticulture.

Impact of climate change on Dutch agriculture

06

The Netherlands is at the forefront of implementing a circular economy in food production. Efforts to reduce food waste are evident throughout the supply chain, from production to consumption. Innovations such as food-sharing platforms, upcycling food waste into new products, and biodegradable packaging are becoming mainstream. This holistic approach not only conserves resources but also creates new economic opportunities.

Circular economy in food production

Real estate implications: The circular economy model is influencing the design and operation of food-related facilities. Industrial and commercial spaces are being repurposed for recycling centres, composting sites, and facilities for producing biodegradable packaging. Mixed-use developments incorporating these elements can attract environmentally conscious businesses and consumers, enhancing the appeal and sustainability of the properties. An example is the initiative Zero Waste Zuidas, aiming to have Amsterdam’s Central Business District waste free by 2030.

05

In addition to plant-based proteins, the Netherlands is exploring other alternative protein sources such as insect-based and lab-grown meat. Companies like Protix are leading the charge in producing insect-based proteins for human consumption and animal feed. Research and development in cultured meat is also progressing, with the aim of providing sustainable alternatives to traditional livestock farming.

Real estate implications: The alternative protein sector requires specialised laboratory and production facilities. Real estate developers can capitalise on this by creating biotech hubs and innovation parks tailored to the needs of alternative protein companies. These developments can attract significant investment and foster collaboration between research institutions, start-ups, and established firms.

Alternative proteins

04

The plant-based movement is gaining significant momentum in the Netherlands. Companies like The Vegetarian Butcher and Beyond Meat are leading the way, providing a variety of plant-based alternatives that cater to both vegetarians and flexitarians. The Dutch government supports this shift through various initiatives aimed at reducing meat consumption and promoting a plant-based diet. This trend is driven by health considerations and a growing awareness of the environmental impact of meat production.

Real estate implications: The growth of the plant-based sector is creating opportunities for specialised manufacturing facilities and distribution centres. Retail spaces, particularly in urban areas, are also adapting to the increasing demand for plant-based products by incorporating more plant-based food outlets and dedicated sections in supermarkets. Property owners can benefit from this trend by leasing spaces to plant-based food producers and retailers. Beyond Meat, a leading producer of plant-based meat, has opened a production facility in Zoeterwoude in collaboration with local player Zandbergen World’s Finest Meat. The collaboration makes it possible to meet the growing European demand for Beyond Meat products. The innovative Beyond Meat products are produced in this ultramodern production location called The New Plant.

Plant-based revolution

03

The Netherlands is a global leader in sustainable agriculture, leveraging advanced agritech solutions to boost productivity and reduce environmental impact. Innovations such as precision farming, vertical farming, and greenhouse technology are integral to Dutch agriculture. These methods not only enhance efficiency but also contribute to food security by enabling year-round production. The use of drones, sensors, and AI in farming practices helps optimise resources and minimise waste, making Dutch agriculture a model of sustainability.

Real estate implications: The demand for high-tech agricultural facilities is rising, driving the development of modern, tech-enabled farms and greenhouses. Investors are increasingly interested in agritech parks and hubs, which can attract both local and international agritech firms. Real estate developers should consider integrating advanced infrastructure to support these technologies, enhancing property values and attracting long-term tenants.

Sustainable agriculture and agritech

02

Finally, DSOs manage the low-voltage grid, the most local layer of the electricity system, which delivers power directly to end users. At this stage, electricity is converted from medium to low voltage (below 1 kV) through local transformer stations, often housed in small above-ground buildings. This final step ensures electricity is supplied at a safe and usable level, typically 230 V, for residential, commercial, and small-scale industrial consumption.

Low-Voltage Grid

Once electricity is transferred from the high-voltage grid to regional substations, it enters the medium-voltage network through transformer substations. These grids operate at voltages between 1 kV and 25 kV and are managed by Distribution System Operators (DSOs). DSOs oversee regional distribution, ensuring that households, businesses, and small-scale producers remain reliably connected to the grid. In the Netherlands, DSOs are publicly owned, often through municipal or regional cooperative structures. The three largest operators are Enexis, Stedin, and Liander. Like TenneT, DSOs are prohibited from selling electricity directly to end users. Instead, they function independently of commercial suppliers and focus on providing regulated, non-discriminatory access to the grid for both producers and consumers.

Medium-Voltage Grid

Source: Municipality of Amsterdam, Kadaster (2025).

Figure 1: Post-war multi-family buildings potentially suitable for optoppen.

The scale and opportunity in post-war building stock

Understanding homeowners’ perceptions and whether their concern is supported by market data is crucial for assessing the feasibility of optoppen. Even if top-floor concerns are addressed, a key questions remains: how many buildings in Amsterdam are actually suitable for optoppen, and how much housing could realistically be added? To asses the potential number of homes, we mapped Amsterdam’s post-war building stock and examined which buildings meet the architectural roof conditions for adding one or more new floors.

Land is scarce, but opportunity is not. Post-war neighbourhoods offer far more potential for growth than we often realise

The result is 1,447 apartment buildings in Amsterdam that are built between 1945 and 1970. Following the optoppen example at the A.J. Ernststraat 800, only horizontal roofs are considered leaving 699 buildings suitable for optoppen. Given approximately 10 apartments can be added per post-war apartment building with a horizontal roof the housing stock could be increased with almost 7,000 homes.

Structural Potential

Although this study did not assess the structural feasibility of each individual building, many post-war buildings offer substantial structural potential. They were often built robustly, frequently on concrete foundations, giving them sufficient capacity for optoppen. Especially since wood / biobased construction is now frequently used, which is far lighter than traditional materials. In the Amsterdam metropolitan area, the housing shortage is currently equal to 76,040 (6.2% of the total housing stock). The estimate of almost 7,000 homes, indicate that the Amsterdam housing shortage could be reduced by 9%, given it is structurally feasible.

Amsterdam’s post-war buildings hold far more capacity than assumed. With suitable roof structures and modern lightweight construction, thousands of new homes could be added, offering a meaningful reduction of the region’s housing shortage.

1,447

post-war apartment buildings mapped across Amsterdam, built between 1945 and 1970.

~7,000

potential homes from optoppen, equal to a 9% reduction.

buildings have flat roofs and are structurally suited for optoppen based on roof typology.

699

Thijs Muller

Founder Creative City Solutions

Utrecht

Take-up (index = 2015)

Average rent

Vacancy

The Hague

Rotterdam

Eindhoven

Mapping the market

examining transaction patters between 2022 and 2025

Between 2022 and 2025, there were 1,062 sales transactions in Amsterdam apartment buildings constructed between 1945 and 1970.

For each sale, detailed information is available on both the characteristics of the apartment (such as number of rooms, EPC label, maintenance condition, presence and type of outdoor space) and the transaction (including asking price, days on the market, and date of sale). Controlling for these features, enables us to isolate the effect of the floor premium as accurately as possible. The figure below shows the distribution of transactions across floor levels in our dataset.

Source: NVM / Brainbay (2025).

Figure 2: Number of transactions per floor level in our sample dataset.

Levi Koppenhol

A systematic comparison of apartment prices across floors allows us to rigorously assess whether higher floors command a premium, or if top-floor units are valued similarly to those below

We also incorporated spatial variables, such as the distance to the nearest public transport, park, and a various amenities, time and neighbourhood fixed effects. Including spatial variables and fixed effects improves the estimates by also capturing neighbourhood- and time-level differences that may influence pricing. Nevertheless, all models are a simplification of the real-world. Therefore, we conducted multiple robustness checks to assess the stability and reliability of our results.

Floor premiums

primarily affected by accessibility rather than exclusivity

Our results show that the price per square metre decreases as floor level increases compared to the ground floor in typical post-war buildings, except for the fourth floor, where prices are slightly higher. To some extent, this can be compared to the way we traditionally view transport costs in geographical location choices. For example, properties closer to the city centre generally command higher prices, because there is shorter commuting time. This also applies vertically with the floor level of an apartment Accessibility Drives Pricing Lower-level apartments have shorter commuting times from the building entrance and greater substitutability between stairs and lifts. However, they are also more exposed to negative environmental issues such as air pollution, noise, limited views, and safety concerns. Higher floors benefit from better views, air quality and greater privacy, but require more effort to reach—especially in buildings without a lift. Thus, there is a trade-off between commuting time and environmental quality. Since typical post-war buildings are originally build without a lift, the floor level premium in our analysis is probably mostly a story about stairs: the higher the apartment is located, the higher the physical effort required to reach it which outweighs the benefits. However, the presence of a lift was not known in our dataset and therefore outside the scope of this analysis. As lift retrofitting is common practice when implementing optoppen by CCS, it is relevant to examine for future research

Why height alone doesn’t add value We expect the presence of a lift will positively impact the floor premium at every floor. With improved vertical accessibility, higher-floor apartments become attractive to a wider range of households, including older residents and families with young children. For future research, it would also be valuable to extend this study to other municipalities to assess whether the findings hold in different contexts. Additionally, examining how rents per square meter are affected by a floor premium would provide further insights in cases the building is owned by a single investor. Nevertheless, our findings show that floor premiums in post-war buildings in Amsterdam are primarily driven by accessibility rather than exclusivity. This means that adding an additional floor does not reduce the price of the existing top-floor apartments, which helps explain why homeowners do not need to fear losing top-level “exclusivity” in terms of value.

What does this mean?

In post-war apartment buildings, the price per square metre decreases as floor level increases compared to the ground floor, except for the fourth floor, where prices are slightly higher.

This pattern exists regardless of whether the building has four or five storeys. For this second finding we examined the interaction effect between the floor level and the type of building: buildings with either a maximum of four storeys or five storeys within our dataset. The floor level premium did not appear to be statistically significantly different for buildings with a fifth floor. In other words, the number of existing storeys in a building does not affect the floor premium at any floor level.

By quantifying how building height affects housing prices, it is possible to model the impact of optoppen and estimate the potential price effects for current homeowners

Our results confirm that the perceived “top-floor exclusivity” is not a price-determining factor, which indicates that adding an additional floor does not erode the value of the current top-floor apartments in typical post-war buildings in Amsterdam.

The table shows how the price per square metre of an apartment varies by floor level and building type. The graph below plots the predicted prices by the model for each floor, holding all other apartment characteristics constant. It shows that ground level and higher-level floors command higher prices.

Source: Savills Data Intelligence and Strategy (2025)

Figure 3: Floor premium / discount in a building constructed between 1945 – 1970 with a maximum of four storeys

Source: Savills Data Intelligence and Strategy (2025).

Figure 4: Interaction between the floor level and type of building

the financial rationale for optoppen

Understanding how floor premiums vary by building type is just one aspect of evaluating the feasibility of optoppen. To get a full picture, it's also crucial to understand how lenders evaluate these projects.

Interviews with RNHB B.V., Rabobank, ANB Amro and Handelsbanken show that lenders view optoppen positively as an innovative means to increase housing supply and support urban densification, provided key conditions are met. Structural feasibility of the existing building and consent from the VvE are the most essential. In general, optoppen projects are assessed using standard redevelopment criteria rather than as a separate financing category. RNHB emphasises that optoppen fit well within standard redevelopment financing, and that structural feasibility and VvE alignment are the most essential prerequisites:

We view optoppen positively. They add supply, create value and fit well within regular redevelopment financing, as long as the project is technically feasible and supported by the homeowners’ association.

RNHB B.V.

Using standard redevelopment criteria, the financial risk is considered similar to entire new build

From a pure financial perspective, all lenders consider optoppen comparable to conventional new builds. Typical requirements include an equity contribution of around 20% and a valuation based on the post-construction value. Also, the risk of vacancy or loss of value for example is comparable to that of regular housing development. Aart Cooiman (Rabobank) continues: “For us, the roof is nothing more than a land position at height.” Rabobank and RNHB expect financing demand to grow and highlight the importance of collaboration with advisory partners and adopting standardised construction methods to scale these projects. The ABN Amro and Handelsbanken, on the other hand, do not expect a rapid rise in financing applications for optoppen, though it hopes demand will grow due to housing supply pressures. VvE complexity, complex permitting procedures and regulations by municipalities are seen as key barriers by both ABN Amro and Handelsbanken, which highlights the complexity of a optoppen project. Sjoerd van Migchelsen (Handelsbanken) believes optoppen is not currently a priority among investors. According to him, growth in financing applications depends on market developments: “In recent periods, funds have been created to support flat exploitations through lower-cost capital. If similar funds are established again in the future, the same would apply.” Overall, the lenders regard optoppen as a viable, socially desirable solution that contributes to housing supply and neighbourhood vitality, provided technical, legal, and financial safeguards are in place. However, their view on the degree of feasibility and future growth varies greatly depending on ownership structure.

ABN Amro adds that a major benefit of optoppen is that existing infrastructure, such as schools and roads, is already in place. The Rabobank sees optoppen as a promising and socially desirable method of spatial development. According to Aart Cooiman (sector specialist in construction and real estate at Rabobank Real Estate Finance), optoppen contribute to enhancing neighbourhood liveability: “Through densification, local amenities gain a broader economic base. Many existing buildings were built for larger families than currently live there; new ‘blood’ is needed to keep neighbourhoods vibrant.”

Aart Cooiman

sector specialist in construction and real estate at Rabobank Real Estate Finance

Through densification, local amenities gain a broader economic base. Many existing buildings were built for larger families than currently live there; new ‘blood’ is needed to keep neighbourhoods vibrant.

The ownership structure: a critical point in terms of feasibility

Although all four lenders view optoppen positively as a contribution to sustainability and densification efforts, they differ in their view on the feasibility of obtaining full consent from the VvE in cases of fragmented ownership. Rabobank positions itself as a frontrunner in financing innovative housing concepts. They are open to supporting and facilitating VvE’s through cooperative structures and are investigating models for distributing revenues equally. The bank views optoppen not just as a construction challenge, but also as a social and sustainable instrument to strengthen existing neighbourhoods. Aart Cooiman says “This is exactly the kind of solution we love helping with as a cooperative bank.”. RNHB is also open to financing in cases of fragmented ownership. However, in such cases fill (upfront) approval from the owners' association is required. Therefore, applications within an owners' association are critically assessed for feasibility and approval. ABN Amro and Handelsbanken distinguishes themselves with a slightly more conservative approach than Rabobank and RNHB regarding fragmented ownership structures. In comparison to fragmented ownership, ABN Amro expect a larger need for credit when a property has a single-owner. Construction costs when ownership is fragmented are mainly financed by split sale-and-construction arrangements resulting in a limited banking role. According to Joram Roozen (senior financing solutions specialist at ABN Amro), the ABN Amro considers the possibility of larger-scale standardisation to be important in reducing construction costs, resulting in better financing propositions. Joram Roozen says: “Larger, more standardised optoppen projects are more attractive to finance, provided the entire property is owned by a single party." Handelsbanken does not finance in cases of fragmented ownership. Sjoerd van Migchelsen (Deputy Branch Manager at Handelsbanken) explains that the bank takes a very personal approach to financing applications, whereby they want to be able to look an owner in the eye and build a long-term relationship. In cases of fragmented ownership (for example with a flat management company of VvE with multiple owners”), they view this is not possible. Sjoerd Migchelsen says: “We view matters through the eyes of the owner. We consider the overall picture and, above all, the final value”

Rabobank, ABN Amro and Handelsbanken link optoppen to energy performance, offering better terms for improved energy labels, while RNHB currently does not provide specific sustainability incentives. Joram Roozen (ABN Amro) explains: “In general, we do not finance non-sustainable real estate without a clear sustainability plan; the level of sustainability is fully reflected in our pricing model.” Sjoerd van Migchelsen (Handelsbanken) continues: “By 2030, we want all our properties to have EPC A. By 2040, we aim to have a net-zero portfolio”

Sustainability

A key criterion for financing conditions for almost all lenders

All content © copyright 2024 Savills. All rights reserved. Savills Nederland Holding B.V., established and registered in the Netherlands. Located: Claude Debussylaan 48, 1082MD Amsterdam. Chamber of Commerce (KvK) number: 33202244.

Savills Data, Intelligence & Strategy Our independent Data, Intelligence & Strategy team solves all of your real estate issues. We work together with developers, investors, municipalities and occupiers and offer them high-quality, highly detailed customized analyses without losing sight of the strategic question. Our advice is based on a solid combination of reliable data and in-depth market knowledge of the various market segments within the real estate market. In our analyses we focus on factors that influence the supply and demand of real estate. The product we deliver always depends on your wishes. We offer a wide variety; from a smart one-pager, an extensive research report to a tailor-made dashboard. Our product will support you in making well-founded property decisions.

Looking ahead

Optoppen as a scalable urban solution

+31 6 114 03965 c.demos@savills.nl

Charlotte de Mos

Head of Marketing & Business Intelligence

Contact

+31 6 214 50535 pascale.schellekens@savills.nl

Market Intelligence Analyst

Optoppen offers a practical, socially and environmentally beneficial solution to Amsterdam’s housing shortage, particularly in post-war buildings. While concerns about loss of “exclusivity” for top-floor apartments exist among homeowners, our analysis shows that this is not a price determining factor. Beyond individual buildings, optoppen contributes to broader urban objectives. They support urban densification, neighbourhood revitalisation, and efficient use of infrastructure. When combined with energy upgrades, they also offer opportunities to significantly improve the sustainability and comfort of the buildings and neighbourhoods. For example, optoppen projects provide a timely opportunity to integrate additional environmental enhancements, such as green roofs or façades, which further enhances the environmental sustainability of neighbourhoods.

By working together towards standardised models, this could become a feasible solution. Collaboration will be essential to realising the full potential of optoppen in the coming years.

Building Upward Toward Amsterdam’s Future

charlotte de mos

Optoppen are not a standalone solution to Amsterdam’s housing shortage, but they represent an increasingly important part of a broader strategy to build within existing neighbourhoods. With a clear understanding of value dynamics, growing interest from lenders and a substantial stock of suitable post-war buildings, the conditions are in place for meaningful scale-up. By combining data-driven insight with collaboration across VvE’s, municipalities, lenders and development partners, optoppen can help deliver new homes where they are needed most - while strengthening the quality and resilience of Amsterdam’s urban fabric

A preliminary mapping of Amsterdam’s post-war building stock suggests that the potential is substantial. With a rough estimate, our sample dataset shown in Figure 1 includes 699 buildings suitable for optoppen. This could add almost 7,000 homes to the housing stock, addressing 9% of Amsterdam’s housing shortage.

For policymakers, homeowners, and lenders alike, these projects present a viable route to expanding housing supply without compromising neighbourhood character or property values. Provided that technical, legal, and financial safeguards are in place.

Claude Debussylaan 48, 1082 MD Amsterdam +31 (0) 20 301 2000

Mon - Fri: 9:00am - 6:00pm

Office opening hours

+31 6 554 74960 b.wilberts@savills.nl

Bas Wilberts

Head of investment